If you are employed for an extended period in Japan, chances are that some of your monthly salary is going to the Employee’s Pension Insurance System. Here’s a guide to navigating this scheme that might seem confusing to many.

If you are employed for an extended period in Japan, chances are that some of your monthly salary is going to the Employee’s Pension Insurance System. Here’s a guide to navigating this scheme that might seem confusing to many.

First, we must differentiate the types of pension insurance Japan imposes. The first is the National Pension Scheme, which is a compulsory premium placed on everyone with a residency or address in Japan, regardless of nationality, as long as you are between 20 and 59 years old.

The National Pension Scheme is further divided into three categories. One is the self-employed, students, and those not in categories two and three. Two are for civil servants, company employees, and those under the Employee’s Pension Insurance System. Lastly, the dependent spouses of those in category two.

The National Pension is a legal and mandatory obligation, with a fixed monthly contribution of around with a fixed monthly contribution of around ¥16,610. You can, however, apply for an exemption per fiscal year for reasons such as insufficient financial capacity, being unemployed, and so on. To do so, you can visit your local city hall, and they will process the exemption within the same day. Those taking maternity leave or childcare leave can also get exempted from paying contributions.

Now, we go into the Employee’s Pension Insurance System or Kosei Nenkin Hoken, which goes hand in hand with the Employee’s Health Insurance, designed to help stabilize the living experience of company workers upon old age, disability, or death.

According to the official website of the Japan Pension Service, these two schemes are compulsory by law and is not a contract for which employers or employees may opt for the coverage or withdraw. Workers, in turn, pay income-based contributions.

On a positive note, if you are employed full-time in a company or factory that has more than five workers, you do not need to register anything to enter the pension system. It is your employer who is responsible for the necessary procedures in enrolling you into the system. Your employer submits an “Application to Enroll in Employees’ Health Insurance or Employees’ Pension Insurance” (Shikaku Shutoku Todoke – Kenko Hoken / Kosei Nenkin) within five days after your employment to the Japan Pension Service branch office or the processing center which handles your company’s insurances.

All foreign nationals must also pay into the system as long as they are permitted to work based on their resident status.

Meanwhile, if you are a part-time worker, you must enroll in the pension system if your weekly work hours and monthly work days are ¾ or more of those for full-time employees in the same workplace. If your hours are less than 75%, enrollment is still mandatory if your condition applies to the five pre-requisites: (1) your weekly work hours are 20 hours or more, (2) your employment term is expected to be two months or longer, (3) your monthly wage is ¥88,000 or more, (4) you are not a student, and (5) you are employed by a “specific covered workplace” such as a company registered under one Hojin (company number) with more than 100 workers at a certain time period. More details can be found here.

You can pay contributions at banks, post offices, or convenience stores using the payment notices sent by the pension office. Those who choose advance payment, automatic bank transfer, or credit card payment can get a discount.

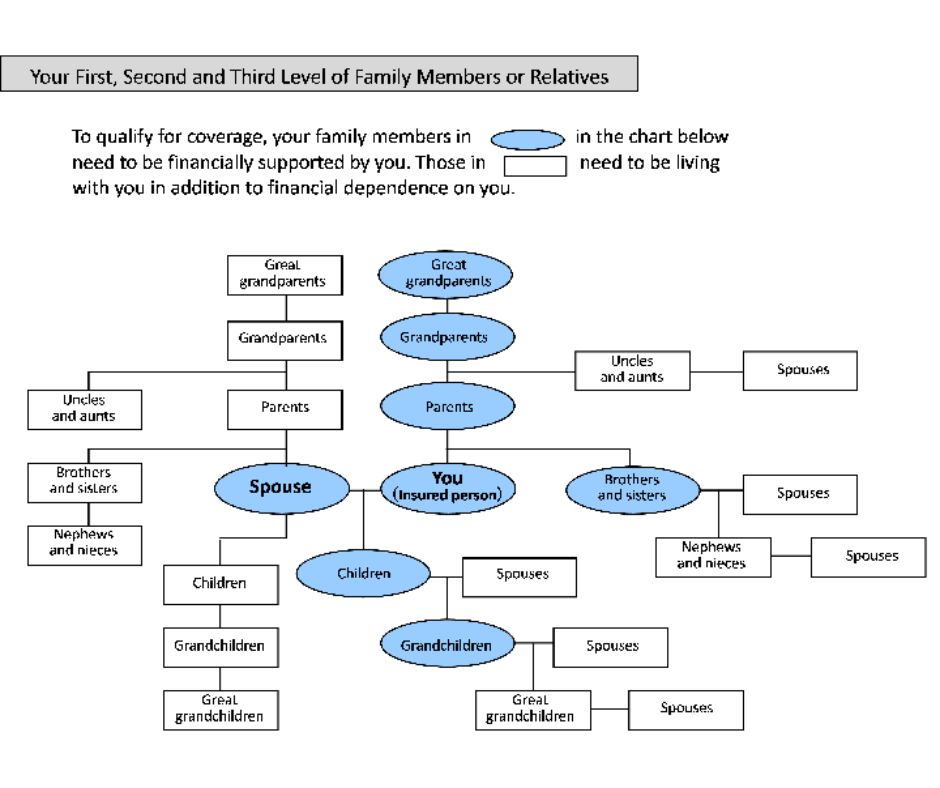

You can also enroll your family members or relatives to be your dependents, as explained in the chart below. They need to have a registered address in Japan and must be financially supported mainly by you. Your dependents must also live with you and earn less than ¥1.3 million a year and less than half of your annual income or less than ¥1.8 million a year if he or she is 60 years old and above or has a certain level of disability.

You and your employer split your contribution amount 50-50 by applying the same contribution rate to your monthly salaries and your bonuses. Half of the amount is automatically deducted from your monthly salaries and bonuses; then your employer pays the full amount by the due date.

Here is the formula:

Contribution amount = your standard monthly salary x contribution rate. To get the contribution amount for bonuses, you add the first contribution amount with your standard bonus x contribution rate.

To start receiving the benefits of your pension payments, you should have to meet certain requirements. For the old-age basic pension, benefits start at the age of 65, and your total contributions paid need to be 10 years or more. The full benefit amount is ¥795,000 per year for fully contributed coverage periods (for 40 years from age 20 to 59). The amount is recalculated for missed periods or exemptions.

To claim your pension, you must apply at your nearest pension office with an official document showing your basic pension number, your pension number notice, your pension handbook, and a certified true copy of your family registry.

Meanwhile, suppose you have one year or more of payments and you are eligible under the contribution requirement. In that case, you can apply for the specially-provided old-age employee’s pension (Tokubetsu Shikyuno Rorei Kosei Nenkin) from your pensionable age (60-64).

If you have paid into the system for 20 years (or 15-19 years after the age of 40, 35 for women), and if you have dependent family members when you reach the age of 65, you can receive additional annual benefits.

Foreigners who will return to their home countries but were enrolled in employees’ pensions can claim remuneration within two years of departure from Japan, as long as they paid at least six months into the system. There is a separate withdrawal of payments form accessible here.

The common perception of the pension scheme is that it is a burden more than a benefit, even among locals, mainly because the payouts are much smaller than the average monthly salary of today and the possible delay in receiving the benefit (the starting age was recently changed from 60 to 65). Japan’s rapidly aging society is another issue that tips the scale regarding workers paying into the system and seniors receiving benefits. However, the whole thing is compulsory, so consider it as extra financial cushioning for the future. I hope the guide helped in explaining the employees’ pension insurance!